Today’s U.S. employment reports have cemented expectations around interest rate policy. Even as Trump aims to steer rates lower by appointing Warsh, strong job growth and rising inflation are instead making it necessary for the Fed to keep rates on hold. Meanwhile, the prolonged Iran conflict is keeping oil prices in the triple digits, fueling energy inflation and driving up costs across the board.

Fed outlooks diverge

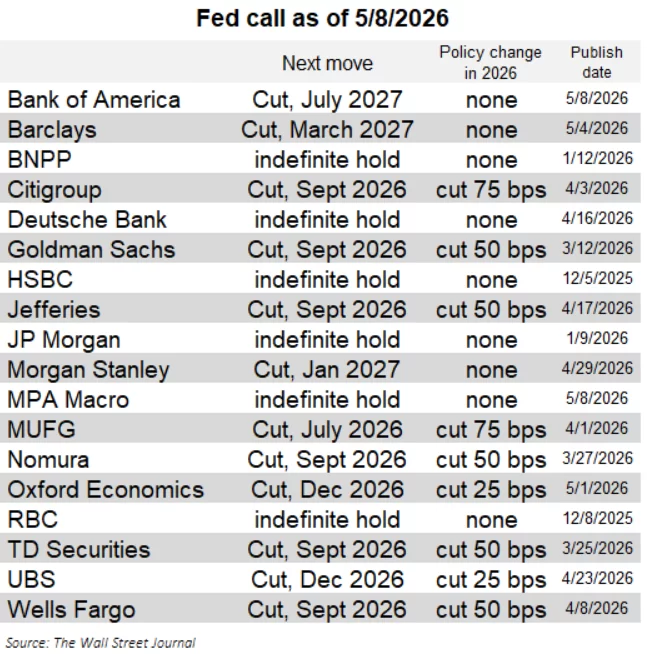

Economist Nick Timiraos has shared the latest interest rate forecasts from leading global financial institutions and research firms, revealing a clear split in expectations for the Federal Reserve’s future rate decisions.

For instance, Bank of America predicts no rate cuts before July 2027, positioning itself among the most hawkish major banks. Barclays does not foresee a cut until March 2027. Other institutions like BNPP, Deutsche Bank, HSBC, JP Morgan, MPA Macro, and RBC also expect rates to remain steady for an extended period.

Sharp disagreements are evident among banks. While some, like Bank of America and Barclays, see no cuts until 2027, others such as Citi and MUFG are anticipating aggressive reductions in the second half of this year. Most expecting early cuts point to September 2026. Citigroup and MUFG remain the most optimistic, projecting as many as 75 cuts in total. These forecasts, however, are highly sensitive to economic shifts, since today’s projections reflect heightened inflation, strong job growth, and ongoing conflict in Iran. Interest rate futures for the U.S. now even price in the possibility of a rate hike in 2026.

“After the release of April’s jobs data, a growing number of investment banks and Fed watchers are removing or delaying rate cuts in their forecasts.” – Nick Timiraos (WSJ)

Some investors argue, “Low interest rates have never caused inflation, and that’s where Warsh would take strong measures. Low rates support growth, and we’ll need that when this ‘orchestrated conflict’ in Iran ends.” Their motivation appears connected to concerns about the cost of U.S. debt.

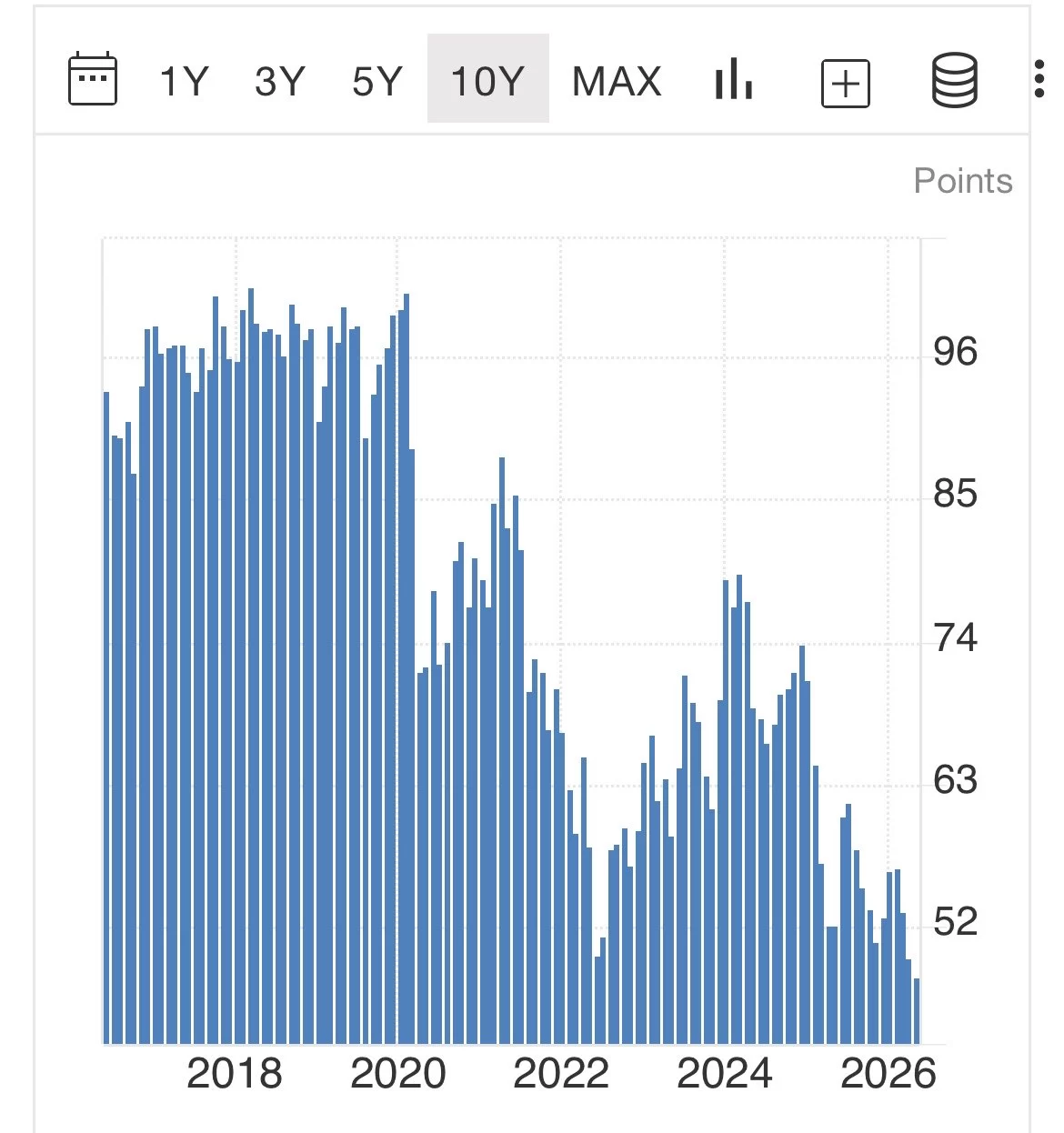

Consumer confidence hits record lows

The Michigan Consumer Sentiment Index has plunged today to a record low of 48.2. This sharp decline underscores how rising prices are undermining personal finances and making large purchases more difficult, with growing anxiety leading Americans to lose faith in the economy. In summary, consumers have little hope for any near-term or longer-term improvement in their financial situation or the overall strength of the U.S. economy.

As American consumers become increasingly pessimistic about the future, the risk that these expectations become self-fulfilling grows. Confidence has not taken a blow this severe in years, painting a worrying picture for risk assets—including cryptocurrencies.

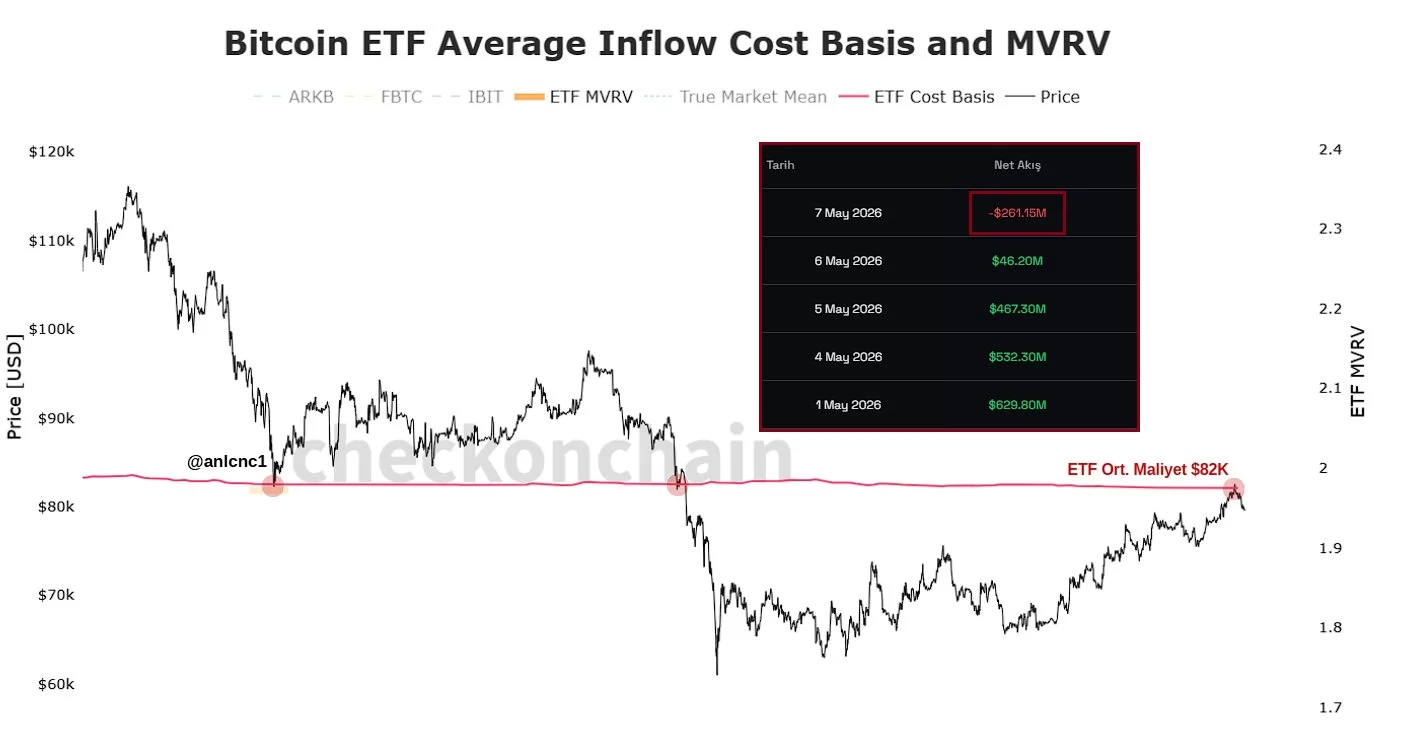

According to @anlcnc1, today’s weakness in the market is linked to holders—including ETF investors—taking profits.

“Yesterday, $261 million flowed out of Bitcoin ETFs. It seems some boomers, seeing prices return to their cost basis, decided that the stress was too much and opted to exit.”

The big question now is: how much longer can the bulls withstand the pressure? The current macro landscape offers no support to risk assets. BTC is struggling to hold the $80,400 level, and combined with these multiple headwinds, fresh lows could be on the horizon this weekend. The next major test may come at $78,000.