The prolonged war involving Iran has already made its mark on US inflation, as reflected in the previous inflation report. Headline inflation surged by 1 percent, effectively undermining the Federal Reserve’s efforts. Now, with the April inflation report about to be released, inflation is still growing, albeit at a slower pace. This situation is increasingly negative for cryptocurrencies. So, what are experts expecting?

US inflation report

On May 12, the US Consumer Price Index (CPI) report will be announced. The Producer Price Index (PPI) is set to follow on Wednesday. For CPI, the annual forecast stands at 3.7 percent, with estimates ranging between 3.5 and 3.9 percent. As for Core CPI, expectations center on 2.7 percent, within a range of 2.6 to 2.9 percent. Should the April CPI come in below these forecasts—especially after March’s sharp jump in overall inflation—stock and cryptocurrency markets are anticipated to benefit.

Because technology stocks, cryptocurrencies, and other risk assets are especially sensitive to interest rate trends, increased market volatility is expected tomorrow no matter the outcome. Should core inflation also rise, another high reading could tighten financial conditions and exert pressure on equity markets. This could prompt the Federal Reserve to contemplate further rate hikes.

Stronger-than-expected inflation data is likely to support the US dollar and bolster expectations that the Fed will remain cautious moving forward.

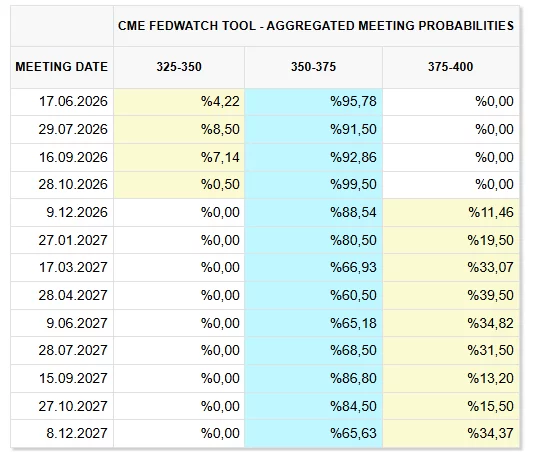

Tomorrow’s report will also shed light on whether recent inflation caused by an energy supply shock was a one-off event. This is the central question. If, as anticipated, the indirect effects start appearing in the data, and if PPI also comes in high on Wednesday, the conversation may shift from rate cuts in 2026–2027 to the prospect of rate increases instead.

US inflation expectations

Analysts at Unicredit expect US CPI to demonstrate robust growth once again. Their forecast for headline inflation has been revised upward from 3.3 percent to 3.6 percent, signaling a return to 2024 conditions when Fed rate hikes were ongoing. A primary driver is gasoline, which increased 12 percent on a monthly basis (or roughly 7 percent when adjusted for seasonality), adding about 0.2 percentage points to headline CPI. Rising jet fuel costs and shortages are likely to push up airline ticket prices, while supply chain disruptions could begin to drive up core goods prices. Analysts will closely monitor how the supply shock affects other categories.

Bank of America anticipates headline inflation at 3.7 percent, driven by a monthly 4.3 percent rise in energy prices. This outlook is even gloomier than Unicredit’s. Core CPI is expected to increase by 0.3 percent monthly and 2.7 percent annually, reflecting a rebound in rents after the recent lull, and persistent inflation in non-housing services. At the time of writing, US markets were trading lower. Trump may deliver remarks at 5:30 PM and 11:00 PM local time, but a comprehensive statement regarding Iran has yet to materialize.

According to Unicredit analysts, the main focus is whether the supply shock begins to spread to other components of the inflation basket, influencing not only energy prices but also jet fuel, airline tickets, and core goods.