In the rapidly evolving crypto landscape, tokenized Real-World Assets (RWAs) have emerged as a dominant theme over the past two years. RWAs refer to the digital representation of tangible assets such as government bonds, money market funds, gold, private credit, equities, and real estate on blockchains. The core aim of tokenizing these assets is to make traditional financial instruments more accessible, programmable, and trackable by leveraging blockchain infrastructure.

Defining Distributed and Represented Assets

The old notion of RWAs as simply “tokenizing an asset” has grown outdated. In March 2026, RWA.xyz introduced a new framework, splitting the market into Distributed Assets and Represented Assets. Distributed Assets are those tokenized assets that can transfer between wallets outside their original issuance platform, emphasizing their mobility. In contrast, Represented Assets primarily use blockchain as a recording and reconciliation layer, but do not circulate freely between wallets. This distinction sheds light on the true scale of “on-chain distribution” in the RWA market.

How Does the RWA Model Operate?

The RWA process begins with the selection of an off-chain asset. Next, ownership, custody, legal compliance, and valuation structures are established. The final step is issuing a blockchain-based token representing the asset. These tokens can stand in for investment rights, fund shares, or claims linked to the underlying asset. Crucially, the token does not replace the physical or conventional asset itself, but digitizes the legal and economic rights associated with it.

This is why RWAs extend beyond mere technical innovation; they drive infrastructural transformation by redefining processes of issuance, custody, transfer, investor access, and reporting. These features have become particularly visible in government bonds, money market products, and credit-based financial instruments, RWA.xyz explained.

Why Do RWAs Matter?

Several factors are driving the rising importance of RWAs. First, moving traditional assets to the blockchain enables 24/7 access, faster settlement, and potentially lower operational costs. Second, costly investment products can be divided into smaller units to broaden participation enabling fractional ownership. Third, when structured legally, tokenized assets can integrate with DeFi and other on-chain finance applications. However, the sector’s promise is not only about boosting liquidity. A common misconception is that tokenization automatically creates deep secondary markets. Both academic research and market data indicate that, for many RWA products, trading volumes, active addresses, and market depth remain limited. In other words, bringing assets on-chain is relatively easy developing truly liquid and robust markets is much more challenging.

The Latest State of the RWA Market as of March 2026

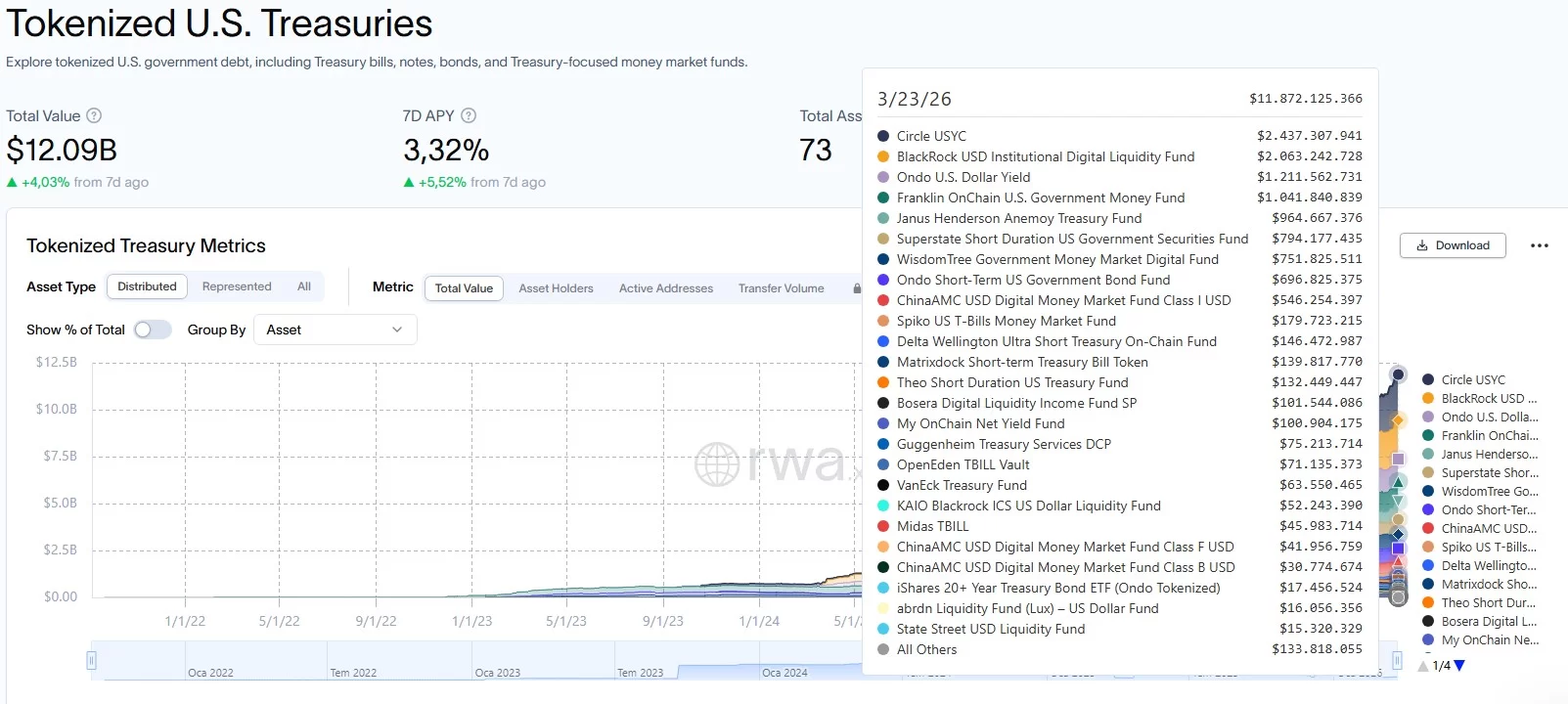

According to data from RWA.xyz, as of March 2026, Distributed Asset Value stands at $26.5 billion, while Represented Asset Value totals $363.78 billion. The number of unique asset holders has reached 692,148. Stablecoins remain a market cornerstone, with a total value of $300.17 billion and 239.71 million holders.

A key takeaway is that the majority of the RWA market still consists of broadly defined assets, with stablecoins making up the lion’s share by scale. Tether (USDT) and USD Coin (USDC) alone account for $185.7 billion and $75.7 billion, respectively together representing most of the stablecoin ecosystem. Therefore, any declaration that “RWAs are growing” should consider how much of that growth comes from stablecoins versus bonds, credit products, commodities, or equity-backed tokens.

Leading RWA Segments and Asset Types

Looking at 2026 figures, tokenized government bonds and money market-like instruments remain among the strongest sub-segments. Standout offerings include USYC at $2.4 billion, BUIDL at $2.1 billion, USDY at $1.2 billion, BENJI at $1.0 billion, and JTRSY at $964.7 million. This trend points to institutional capital favoring short-term, predictable-yield instruments with clear regulatory frameworks.

On the commodity front, gold leads the pack. RWA.xyz lists XAUT with $2.6 billion and PAXG with $2.2 billion in assets showing steady interest in blockchain-traded products backed by physical gold prices. In short, the notion of RWAs as “safe havens” applies not only in traditional markets, but also in tokenized commodity segments.

The equity segment, while smaller, is drawing attention for its growth potential. Products like CRCLon ($127.6 million), EXOD ($73 million), TSLAx ($49.6 million), and COINon ($41.8 million) are included in the data. Although far from the scale of bonds or stablecoins, such offerings highlight the symbolic importance of bringing stock market assets on-chain and signal that the next RWA growth wave may come from tokenized equity and fund infrastructure.

Which Blockchains Are Shaping the RWA Ecosystem?

Ethereum stands out as the clear leader in network distribution. RWA.xyz reports 562 RWAs live on Ethereum, with a total value of $15.3 billion accounting for 57.75% of the market. BNB Chain follows with $3.2 billion, then Solana ($1.7 billion), Stellar ($1.4 billion), and Liquid Network ($1.3 billion). Notably, BNB Chain saw a 36.51% increase in distribution over 30 days, and Plume posted a 69.26% jump, showcasing rising interest in alternative chains.

While this data confirms that the RWA market is not chain-exclusive, Ethereum still dominates in institutional perception, liquidity, and asset variety. Growth on other networks seems driven by lower costs, targeted platform partnerships, and region-specific use cases.

Top Platforms and Issuers in the RWA Space

Among RWA platforms, Securitize leads with $3.04 billion in assets (excluding stablecoins), backed by 21 RWA products and 1,790 holders solidifying its status as a major institutional tokenization provider. Other prominent names include Maple, Circle, Paxos, Centrifuge, Spiko, Libeara, and Franklin Templeton Benji Investments. On the asset management side, Maple Protocol Pool Operations ($2.71 billion), Tether ($2.56 billion), Circle ($2.44 billion), Paxos ($2.23 billion), BlackRock ($2.17 billion), and Ondo ($1.91 billion) top the rankings. The visibility of legacy finance giants like BlackRock and Ondo signals that interest in RWAs now extends well beyond crypto-native startups.

Risks and Limitations of the RWA Model

Despite strong momentum, the RWA sector faces notable risks. Each tokenized asset requires a solid legal framework, custody solution, and transparent reporting system. Even if a token exists on-chain, its underlying value depends on the issuer’s credibility and regulatory positioning. Investor access often remains gated by whitelists, compliance checks, and regional laws. As a result, even “on-chain” RWAs may not offer the fully open, borderless experience that decentralized finance envisions.

Ultimately, RWAs stand as one of the most tangible bridges between blockchain and real-world economies. The representation of traditional assets such as bonds, gold, credit, equities, and real estate on-chain could significantly reshape capital markets in the medium term. Data from March 2026 reveals the market’s evolution from a niche experiment to a multi-billion dollar domain with hundreds of thousands of asset holders and an influx of institutional players. Nevertheless, stablecoin dominance, the distinction between distributed and represented assets, and the true state of market liquidity remain crucial factors for interpreting the sector’s progress.