This week has been especially eventful for cryptocurrencies, with increased moderate statements today fueling a slight uptick in Bitcoin prices. While Trump’s declining momentum in the polls has coincided with sharp losses in related tokens, all eyes are now turning to a host of critical events—chief among them tomorrow’s U.S. inflation data. Meanwhile, the situation involving Iran continues to inject volatility into global markets. Over the next 48 hours, 17 significant developments are set to shape market directions, making it essential for traders to stay alert and responsive.

Regional Tensions Ripple Across Markets

The conflict involving Iran remains a persistent source of instability for global energy and financial markets. Reports emerged this evening of mines being deployed in the Strait of Hormuz, briefly unsettling markets before tensions subsided. While some U.S. intelligence sources lent credence to the story, former President Trump not only denied the reports but also suggested that no such intelligence assessment existed.

The S&P 500 erased earlier gains after U.S. Energy Secretary Chris Wright’s since-deleted social media post, which indicated that no tankers had successfully navigated the Strait, was rebuffed by the White House. U.S. crude oil prices, which had plummeted below the $80 mark during the turmoil, managed to rebound as the situation calmed.

As the Iran-U.S. confrontation enters its 11th day and military actions intensify, the White House states it is considering all available tools to stabilize oil prices. The G7 has also called on international energy agencies to prepare scenarios for releasing emergency reserves. Tensions in the region, therefore, are far from over, and any escalation will likely send fresh shockwaves across global markets.

Countdown to Key Economic Indicators and Blockchain Milestones

The next 48 hours will see a succession of market-moving events. Foremost among them is the anticipation of updates from Iran, but the timeline extends much further. Beginning just after midnight, the Oracle earnings report is expected—a development that could refuel the debate around the so-called “AI bubble” if results disappoint, possibly leading to late-session sell-offs across risk assets.

Later tonight, Japan’s Producer Price Index is set for release. After last year’s carry trade turbulence, market watchers will be hoping for a modest 2.2% increase; any deviation may revive speculation that Japan could raise rates, unsettling global risk markets once more.

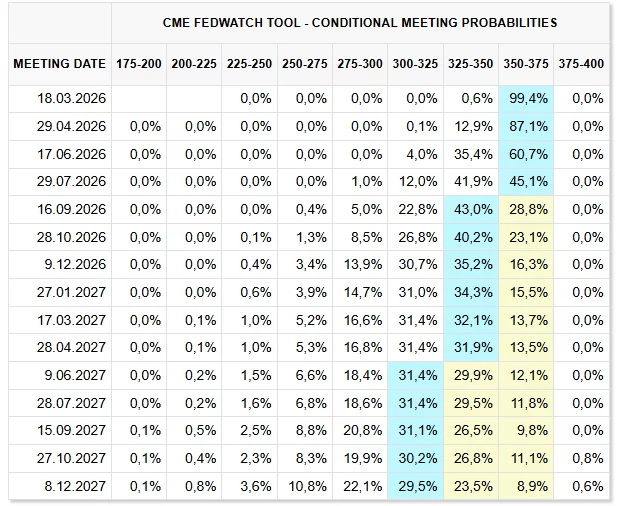

One hour ahead of the U.S. market open, both the Core Consumer Price Index and headline inflation numbers for the U.S. will be published, with consensus forecasts at 2.5% for each. The full impact of recent energy price swings will reveal itself next month, but for now, markets are hoping inflation stays below estimates to keep further pressure off the Federal Reserve. Persistent inflation—especially if compounded by rising oil prices—could postpone any rate cuts well into 2026.

For now, a single rate cut remains largely priced in. Later in the day, remarks from Fed Governor Bowman will be closely monitored for signs of a policy shift. Meanwhile, the Qubic Network Guardians platform enters open beta on Wednesday, and the UK’s House of Lords nears its deadline for gathering evidence related to stablecoin regulations—a crucial step in the evolving regulatory landscape.

Thursday kicks off with the Central Bank of the Republic of Turkey’s interest rate decision, bearing significant implications for TRY-denominated crypto trades—especially with energy costs rising. American jobless claims follow, and another appearance from Fed Governor Bowman is scheduled later in the day. On the crypto side, Aptos is releasing 0.69% of its token supply from lockup on March 12, a move that could influence both volatility and liquidity for the project.

Illuvium’s Illuvitar event, Wave 5, launches on Thursday, but the largest anticipated altcoin development comes from Polkadot. DOT’s supply will be capped at 2.1 billion, emission rates slashed by 53.6%, and the unbonding period drastically reduced from 28 days to as little as 24–48 hours. Such changes could inject significant activity and volatility into the altcoin landscape throughout the coming days.

Elsewhere, Apecoin is set to introduce an agent API—an effort aimed at reviving metaverse engagement. Snapshot eligibility for RNGR holders will be determined at 16:00 PST on March 12, while MetaDAO is preparing a USDC airdrop approaching $5 million in value.

Ending the week, the UK Financial Conduct Authority’s CP26/4 consultation phase concludes, delivering much-anticipated guidance for crypto asset firms. Coupled with parliamentary scrutiny of stablecoins, investors and industry stakeholders should be prepared for waves of market-moving news out of the United Kingdom in the days ahead.