While Turkey’s focus turned to its national football team securing a spot in the World Cup, the country’s cryptocurrency investors received disappointing news. The long-anticipated crypto tax bill has passed through parliament’s committee stage with almost no changes, maintaining contentious requirements for users of international exchanges. For investors hoping for amendments, the legislation’s progress marks an unwelcome development at a pivotal moment.

Community hope dashed after earlier withdrawal

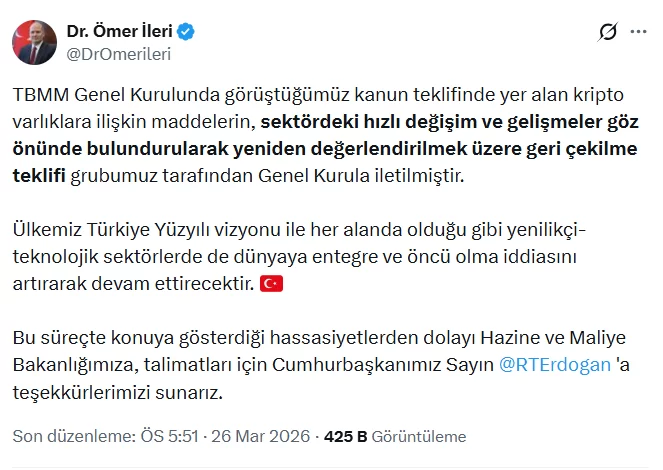

Expectations that the bill would be revised were bolstered when Ömer İleri, Deputy Chairman of Turkey’s ruling AK Party and head of Information and Communication Technologies, briefly announced the withdrawal of the crypto provisions several months ago in response to strong community feedback. Investors saw this as a sign that lawmakers would seriously consider the public’s concerns about the proposed regulations. On March 26, İleri addressed citizens with the following remarks:

“We have submitted a proposal to withdraw the articles on crypto assets from the draft law being discussed in the Grand National Assembly, so that their implications can be reconsidered in light of rapid developments in the sector.

Turkey will continue to pursue its vision of being globally integrated and leading in innovative technology sectors.”

Despite İleri’s statement suggesting that a softer approach to crypto regulation could be on the table, the latest draft approved by the Planning and Budget Committee just hours earlier suggests otherwise. The document shows that almost all provisions remained intact, leaving little room for optimism among investors and market participants.

Taxation rules spark uncertainty for crypto investors

Although it was initially promising that lawmakers appeared to take the concerns of more than 10 million Turkish crypto investors into account, the final version of the bill that cleared the committee has led to disappointment. Turkey had a genuine opportunity to strengthen its position as a global crypto hub—especially after recent geopolitical tensions in the Gulf, such as the Iran conflict, began to erode the appeal of competing destinations like Dubai. With billions of dollars of crypto wealth in play, Turkey could have attracted both investors and blockchain startups—but the bill’s provisions instead threaten to push homegrown users and capital abroad, as the specter of taxes as high as 40% on overseas transactions looms large.

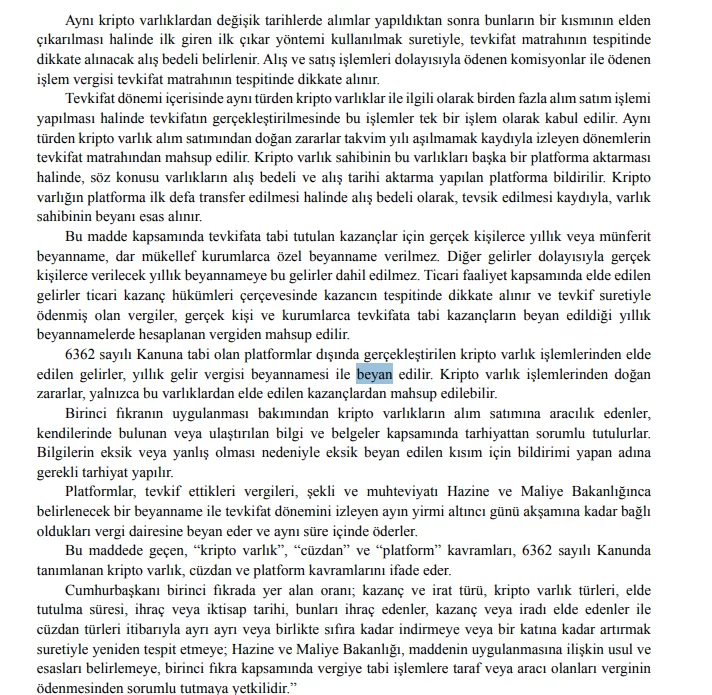

Under the finalized legislation, a 0.03% transfer tax is set to be charged on certain crypto transactions, while a 10% withholding tax will apply to trades on local Turkish exchanges. Those with accounts on global exchanges not under the supervision of Turkey’s Capital Markets Board (SPK) face an additional burden: they will be required to file annual income declarations for their crypto earnings—a compliance hurdle many investors view as especially onerous.

Many had hoped that a more flexible or phased tax policy would emerge from parliament, particularly after the legislation was briefly recalled earlier in the year. However, market participants now face tough choices. Some may be forced to move their investments to more favorable jurisdictions, while others may reconsider their involvement in what was once seen as a promising local crypto market.

The timing of the bill—signed off as the nation celebrated a major football triumph—has not gone unnoticed by the crypto community. Many investors were caught off guard, as attention was focused almost exclusively on sports rather than policy developments. The abrupt passage through committee has left stakeholders scrambling to understand the full ramifications for their holdings and businesses.

As Turkey moves forward with its new regulatory approach to digital assets, it will have to balance the goals of tax compliance and international competitiveness. Whether the current form of the bill will encourage innovation or drive investors away remains a point of heated debate. What is clear is that the legislation, largely unchanged from its contentious original draft, has done little to ease concerns among local crypto users and entrepreneurs.