Certain Federal Reserve meetings always command more attention, often signaling coming changes in monetary policy. While the Fed’s March 18 meeting may not carry the same high stakes as its most pivotal gatherings, analysts say its significance is heightened this time by the ongoing Iran conflict. This week, central banks in Japan, Europe, and the United States are expected to grapple with mounting inflationary pressure in food and energy prices tied to the war’s disruptions.

Markets Brace for a Cautious Fed Stance

Market consensus points clearly to the Fed leaving interest rates unchanged in March. All eyes are now on the Summary of Economic Projections and the press conference with Chair Jerome Powell, which could deliver surprises. While a rate cut is extremely unlikely—and would trigger an immediate rally in cryptocurrency markets if it did occur—the scenario baked into asset prices points to a steady policy with hints at just one rate cut slated for 2026. Powell’s tone and any signaling of future policy shifts remain key variables for the financial markets.

Inflation Outlook Influences Timing of Rate Shifts

Investors will parse every detail of the Fed’s dot plot and economic projections, hoping for clues on when rates might eventually fall. Strong growth or stickier-than-expected inflation could prompt the Fed to keep policy tighter for longer, while clear progress toward 2% inflation might open the door to earlier cuts. Yet, with heightened geopolitical tensions stemming from the Iran conflict, an accelerated easing path now seems very unlikely.

Barclays expects rates to hold steady, noting that at least two policymakers may favor a dovish stance and formally note their dissent. Updated projections may reveal somewhat higher inflation and modestly stronger GDP growth for 2026, but major shifts in unemployment assumptions are not anticipated. According to Barclays, the Fed is expected to telegraph a single 25-basis-point cut in both 2026 and 2027, with projections for 2028 likely remaining unchanged.

During the press conference, Powell is expected to reiterate the Fed’s patience, Barclays said, suggesting that officials will cite geopolitical dynamics, extra inflation pressures, and weak economic activity as concerns. The overarching message should be that policy remains well-positioned to manage risks to both sides of the dual mandate, with decisions continuing to be taken on a meeting-by-meeting basis. Rate cut expectations have shifted, with markets now anticipating a cut in September instead of June, and another in March 2027 rather than December. This assumes core inflation remains moderate and oil prices ease later in the year, implying just one rate cut of 25 basis points in 2024 and another in 2027, should inflation cool further.

With Warsh unlikely to upend current projections upon taking office, Barclays anticipates the Fed will remain unmoved by pressures to accommodate political interests in the coming quarters.

Bank of America also forecasts the Fed will keep rates steady. The firm’s analysts expect an 8–2 vote, with Miran and Waller dissenting in favor of a 25-basis-point reduction.

Bank of America notes that the policy statement will likely reference the Iran conflict, possibly by strengthening language about economic uncertainty and highlighting that a sustained rise in oil prices could push inflation higher while also undermining economic growth.

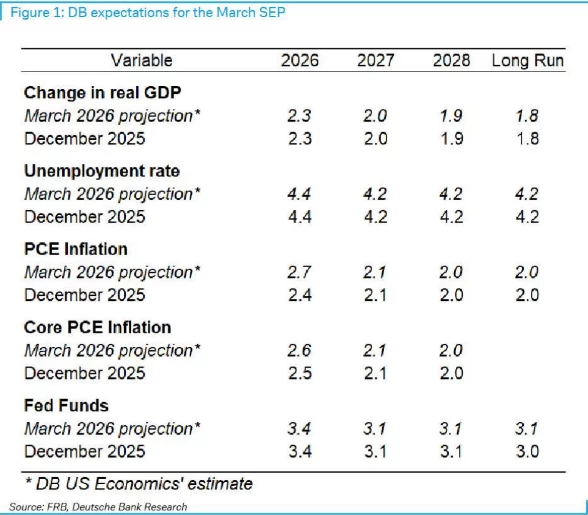

Deutsche Bank likewise sees no shift in the Fed’s stance, with Iran’s situation reinforcing the case for policy continuity. Powell is not expected to hint at near-term moves, making it almost certain that rates will remain unchanged through April as well.

Deutsche Bank explains that the Summary of Economic Projections should reflect only modest revisions to headline and core PCE inflation for this year, while growth and employment forecasts will likely stay near previous levels, given limited new data and heightened uncertainty. Expectations are for slightly higher core PCE, owing to a stronger start to the year on inflation and a mild pass-through from rising energy costs. The median dot still points to one rate cut in 2026, with a minor upward shift in long-term projections.