In the wake of former President Donald Trump’s national address, expectations for the trajectory of the US economy through 2026 have shifted significantly. Trump’s remarks have also cast a shadow over sentiment in cryptocurrency markets, dampening forecasts. Meanwhile, a pre-address report issued by the International Monetary Fund (IMF) sheds important light on how US macroeconomic factors may play out in the years ahead—raising questions about the Federal Reserve’s next moves and the implications of possible leadership changes.

IMF outlook spotlights growth, inflation, and risks

The health of the US economy holds profound significance for global markets, including the evolving world of cryptocurrencies. As cryptocurrencies mature into mainstream asset classes, they have become more exposed to the swings and shocks of global economies. The IMF, in its latest report released just before Trump’s speech, offers a clear snapshot of anticipated trends: In 2025, the IMF expects US inflation to remain stable, driven by tariff-related increases in goods prices, while services inflation stays moderate. The impact of elevated tariffs should begin to subside, and a decline in oil prices is anticipated. After a 2 percent GDP growth in 2025, the IMF projects an uptick to 2.4 percent in 2026, reflecting these more benign trade and energy conditions.

Energy prices and fiscal policy: underlying risks

Despite relatively balanced short-term risks related to economic activity and unemployment, the IMF warns that sustained volatility in global energy markets could fuel upside risks for inflation. The current trend of slower job growth—less than half the pace seen in the five years prior to the pandemic—adds to these concerns. Another challenge: while changes in tariffs and fiscal policy might narrow the current account deficit slightly to around three percent of GDP in the medium-term, public sector deficits are projected to stay high, ranging from 7 to 7.5 percent of GDP, with federal debt rising past 140 percent of GDP by 2031.

Although the IMF is hopeful that core PCE (Personal Consumption Expenditures) inflation can return to the 2 percent target by early 2027, Trump has downplayed the importance of global conflicts such as the ongoing wars, even if they were to end soon. He indicates the underlying drivers of energy prices—including war-related pressures on oil—will likely persist for months, potentially keeping inflation elevated.

Trump’s comments come as US gasoline prices have topped $4 per gallon for the first time since 2022, drawing criticism from the public. In response, Trump suggested that concerns about more severe threats, such as potential nuclear conflict with Iran, justify his administration’s priorities—even if those choices entail risks of higher inflation or the need for tighter monetary policy. This stance suggests the administration could be prepared for higher interest rates rather than urgent rate cuts.

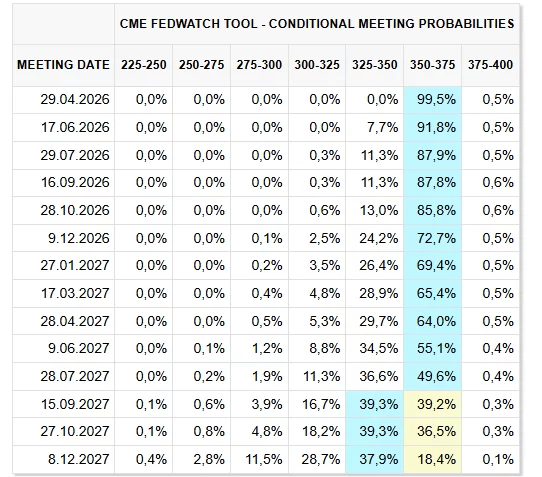

For cryptocurrency investors, these shifting expectations have significant implications. At the start of the year, the market had largely anticipated a return to monetary easing in the US and abroad. Yet, with the European Central Bank hinting that any change to rates would likely mean increases—not cuts—and the Fed in no rush to lower rates, holding rates steady now appears the most probable path. The FedWatch tool now signals that meaningful rate reductions may only materialize in 2027 at the earliest, muting hopes for an earlier dovish pivot.

The inflationary impact of oil prices above $100 per barrel will soon be reflected in official reports, with key data scheduled for release on April 10. As rising fuel prices from March work their way into inflation metrics, the probability of the Fed raising rates in 2026, once thought remote, may rise notably. With Trump stating that military actions are likely to persist for several more weeks, elevated inflation could continue into the spring, sustaining a hawkish monetary environment.

For now, the most likely scenario confronting cryptocurrencies is that sustained inflation and stagnant monetary policy will dampen performance, as risk markets price in persistent pressure. The tangible impact of war is already showing up around the world, from increased food transport costs in Turkey to rising fertilizer prices. In the United States, whereas policymakers used to fine-tune strategies based on small oil price changes, the current environment—with swings of tens of dollars per barrel—poses a serious challenge for risk assets. The anticipated swearing-in of Kevin Warsh as Federal Reserve Chair in May is unlikely to bring a dramatic shift: available data and the outlook for inflation both suggest that meaningful rate cuts are off the table while inflation remains high.

US West Texas Intermediate (WTI) crude oil futures closed at $111.54 per barrel—the fastest rise (12.8%) since 2020 and the highest price since June 2022. The rally, which has been building over the last month, adds further headwinds for policymakers and risk markets alike.