The SEC, the U.S. securities regulator, has maintained a negative stance toward cryptocurrencies for years. As confirmed and criticized by SEC members like Hester, the current administration’s approach denies cryptocurrency companies the opportunity to thrive within the U.S. Furthermore, the CEO of the Blockchain Association has warned cryptocurrency investors about ongoing regulatory challenges.

AAPL

AAPLSEC and Cryptocurrencies

Last June, the SEC initiated lawsuits against exchanges Binance and Coinbase, marking a turbulent week. The institution, led by Gary Gensler, has taken a strong stance against cryptocurrencies among regulatory agencies under the Biden administration. Gensler is expected to leave by March next year, with Trump stating, “I will fire him on my first day.”

SEC lawsuits primarily focus on a singular assertion: “cryptocurrencies are securities/investment contracts and do not comply with regulations.” However, there’s a significant problem here. Cryptocurrency companies cannot meet the SEC’s desired legal compliance requirements due to the ambiguity surrounding the agency’s specific legal demands. While the SEC has imposed registration requirements for tokens, it fails to provide clear guidance on how these projects can register.

SEC May Make a Significant Move This Year

Today, the Blockchain Association’s CEO noted that the SEC’s fiscal year ended on September 30, suggesting we may see further SEC actions in the coming weeks. This implies that we could witness swift legal actions against cryptocurrency exchanges, DeFi projects, and tokens shortly.

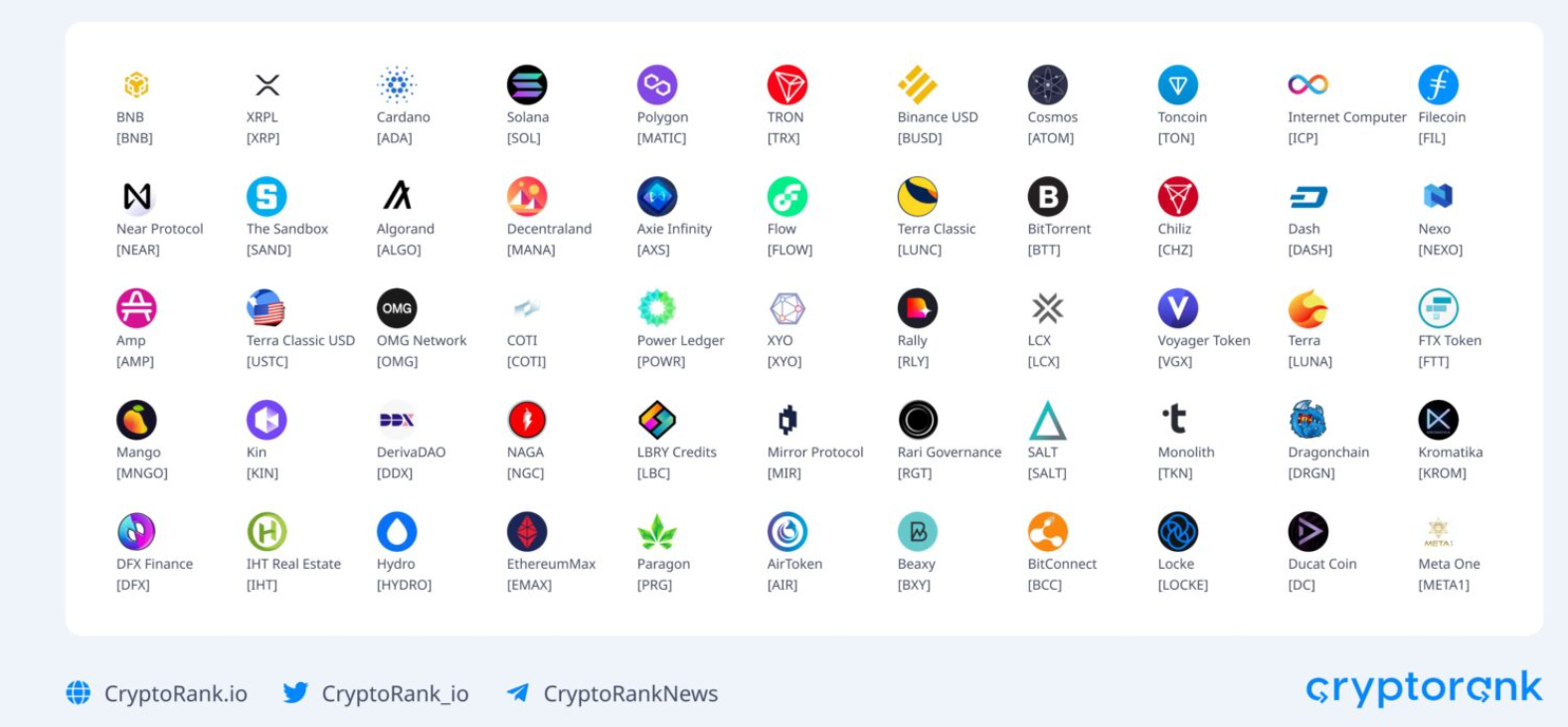

Previously, investors have seen lawsuits involving ATOM, BNB, BUSD, CHZ, NEAR, FLOW, ICP, SOL, MATIC, FIL, SAND, MANA, ALGO, AXS, and around 100 other cryptocurrencies, most of which are altcoins involved in the Binance and Coinbase lawsuits.