This week, investors and analysts in the United States are closely tracking employment data, with the first major jobs report of the week released just moments ago. The JOLTS report sheds light on the current trend in job openings, providing a window into the labor market’s supply side. Meanwhile, figures for the Conference Board’s Consumer Confidence Index are also watched to assess how ongoing global conflicts could be weighing on household sentiment.

Job market trends and consumer sentiment

According to forecasts, job openings as measured by JOLTS were expected to fall from last month’s 6.946 million to 6.89 million. Alongside this, the Consumer Confidence Index was anticipated to dip from November’s reading of 91.2 to 87.9. Another notable development was the price of gasoline surpassing $4 a gallon for the first time since 2022, setting a challenging stage for political leaders such as Donald Trump as midterm elections approach.

Key figures from the latest reports

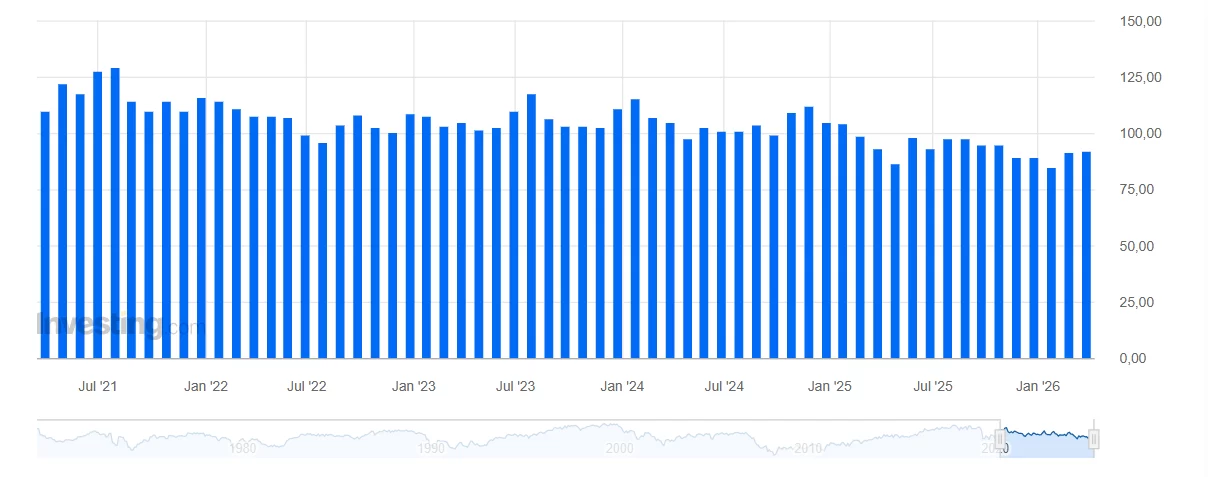

The newly released data confirmed a mild downturn in job openings, with JOLTS reporting 6.882 million—slightly below the 6.89 million consensus and last month’s 6.946 million. Consumer confidence, however, came in unexpectedly strong at 91.8, outperforming the 87.9 projection and last month’s 91.2 figure. Despite the expected softening in the job market, the resilience in consumer sentiment signals ongoing optimism among American households.

The consumer confidence report reveals that both the average and median 12-month inflation expectations remain elevated, though little changed from previous surveys. Respondents also forecast that interest rates will stay at historically high levels over the coming year, reflecting persisting concerns about borrowing costs and the broader economic environment.

“The Present Situation Index fell by 9.5 points in December to 116.8. The Expectations Index, which is based on consumers’ short-term outlook for income, business, and labor market conditions, held steady at 70.7. For the eleventh consecutive month, the Expectations Index remained below 80, a threshold commonly seen as signaling recession risk in the near term.”

Dana M. Peterson, Chief Economist at The Conference Board, elaborated on the month’s results and the factors influencing sentiment.

“Despite an upward revision in November related to the resolution of the government shutdown, consumer confidence declined again in December and now remains well below the peak reached in January of this year. Four out of the index’s five components fell, with one indicator at levels that suggest pronounced softness.

Household survey responses continued to highlight concerns about prices and inflation, tariffs and trade, and political issues as the main factors affecting their economic outlook.”

The January report appears to mark a stabilization in the Consumer Confidence Index following a sustained period of decline, suggesting that the index may be forming a bottom after months of deterioration.