The outlook for cryptocurrencies at the start of 2026 was already bearish, with many predicting a difficult first quarter. However, the outbreak of war has clouded prospects for the remainder of the year as well, prompting renewed fears of interest rate hikes by the Federal Reserve, rather than the rapid rate cuts investors had previously hoped for. So how do JPMorgan analysts currently assess the evolving situation in the digital asset markets?

JPMorgan’s latest cryptocurrency market report

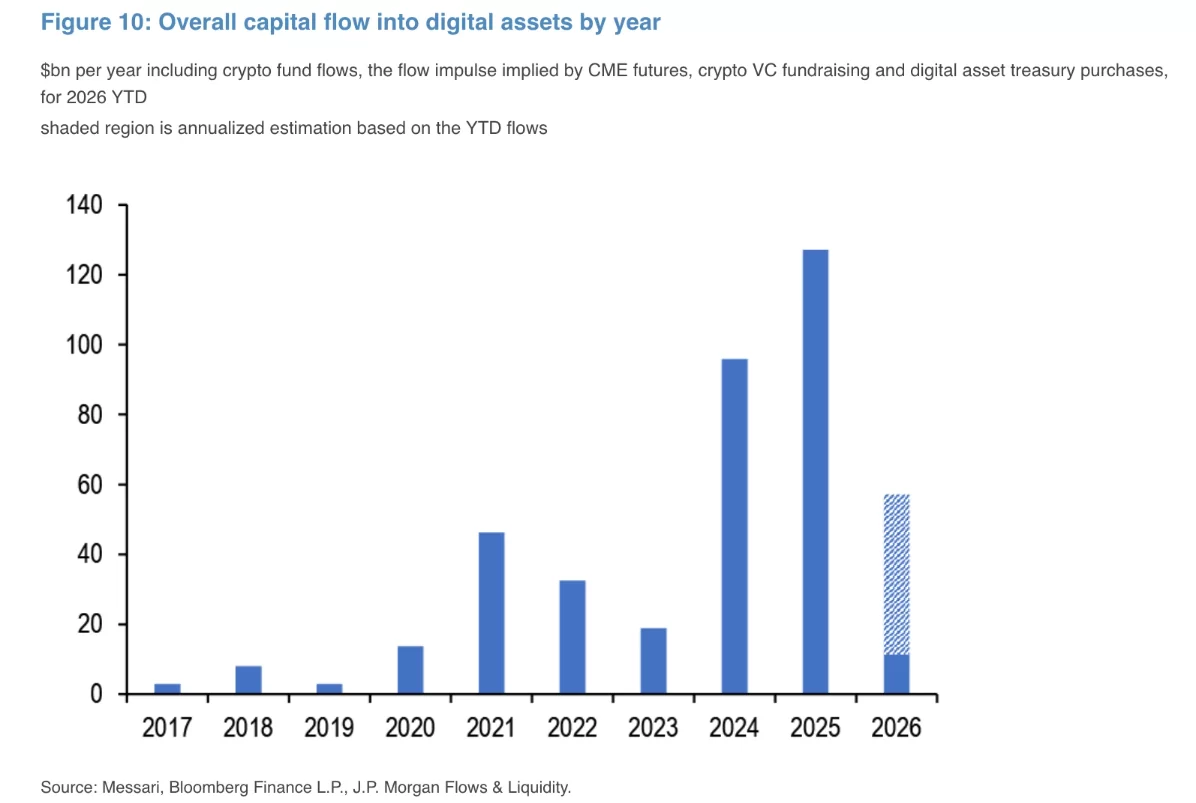

Yesterday’s review highlighted weaknesses in spot demand, and despite occasional increases via exchange-traded funds (ETFs), these have lacked consistency. JPMorgan analysts confirm that demand for cryptocurrencies declined significantly entering the new year. Over the past three months, net inflows to digital assets amounted to around $11 billion, reaching only a third of the levels seen in the first quarter of 2025.

If conditions fail to improve and inflows continue at their current pace, projections for total crypto inflows in 2026 max out at $44 billion, a dramatic drop from the $130 billion amassed last year. Analysts attribute their calculations to a composite view, aggregating flows through the ETF channel, CME futures activity, crypto venture capital investment, and major institutional treasury purchases led by companies such as Strategy. According to the latest report, headed by Managing Director Nikolaos Panigirtzoglou, open interest in CME futures weakened considerably compared to 2024 and 2025. This suggests that overall institutional demand through futures has turned negative so far this year.

The decline in institutional buying has been a key driver behind the lackluster first-quarter performance. In the words of JPMorgan analysts led by Panigirtzoglou,

“In the first quarter of 2026, Strategy’s Bitcoin accumulation was primarily funded through stock issuance. The company has stated its intent to continue using a mix of common stocks and perpetual preferred shares to support ongoing Bitcoin purchases, while other corporate treasuries maintained a more defensive posture.”

This aligns with earlier observations that growing risks and waning interest among treasury buyers meant that, apart from Strategy, few were actively purchasing Bitcoin. On the Ethereum side, BitMine stood out as one of the scarce institutional buyers. By November, even funds such as ETHZilla had begun liquidating their crypto holdings to invest in traditional equities, underscoring the market’s defensive shift.

Sell pressure extends to mining companies

In the first three months of 2026, publicly listed Bitcoin mining firms became net sellers, coinciding with a steep decline in network difficulty. Some major miners have even begun redirecting their computational resources toward artificial intelligence applications—a shift seen as a threat to the sector’s long-term viability. JPMorgan’s analysts note that these sales have been driven not only by market concerns but also by companies moving into AI ventures.

“As a result, our estimate for total digital asset flows decelerated markedly in the first quarter, running at nearly a third of last year’s pace. Both retail and institutional investor flows have remained muted since January, even dipping into negative territory. The majority of digital asset inflows so far this year have stemmed from Strategy’s Bitcoin purchases and concentrated VC investments in crypto.” – JPMorgan

The combination of faltering institutional demand, declining retail flows, and the repositioning of mining firms has intensified the headwinds facing cryptocurrency markets. These intersecting factors underscore a critical transformation in both the participation and structure of the digital asset space as 2026 unfolds.

With traditional corporate treasuries and even key institutional players retreating, the engine of demand increasingly relies on a handful of dedicated entities, most notably Strategy. The shift to preferred equity as a funding mechanism further signals a more cautious and fragmented market landscape.

Meanwhile, the movement of mining resources toward AI and adjacent sectors reveals new priorities for some of the digital infrastructure backbone. This pivot may diminish mining output, exerting additional pressure on both supply and sentiment within crypto ecosystems.

Looking ahead, analysts suggest that only a rebound in macroeconomic conditions or a shift in global risk appetite might stabilize or revive flows into digital assets. As it stands, 2026 presents a more challenging environment for the crypto sector compared to recent years, with broader market uncertainties likely to shape its trajectory for months to come.