The U.S. 401(k) retirement plan system, a primary vehicle for private sector employees to save for retirement with tax benefits, is undergoing significant changes. With recent regulations introduced during the Trump administration, 401(k) participants can now access cryptocurrency investment options, marking a pivotal development for both retirement savers and the crypto market. As new rules take effect, there is growing anticipation within the investment community about what this might mean for the scale and direction of retirement savings in the United States. But what exactly is the 401(k) system, how large is this market, and what scale of crypto investments might these plans attract?

The 401(k): America’s employer-backed retirement system

Comparable to Turkey’s Individual Pension System (BES) and its Automatic Enrollment Scheme (OKS), the U.S. 401(k) is designed to help employees build retirement savings, often through regular deductions from their paychecks. In a structure echoing newer approaches elsewhere, U.S. employers frequently match a portion of workers’ contributions—effectively boosting employee savings—whereas in Turkey, the state provides matching contributions. There are two main 401(k) types: traditional plans allow for pre-tax contributions with taxes paid upon withdrawal, while Roth 401(k)s involve after-tax contributions, making qualifying withdrawals tax-free in retirement.

The scale of the 401(k) market

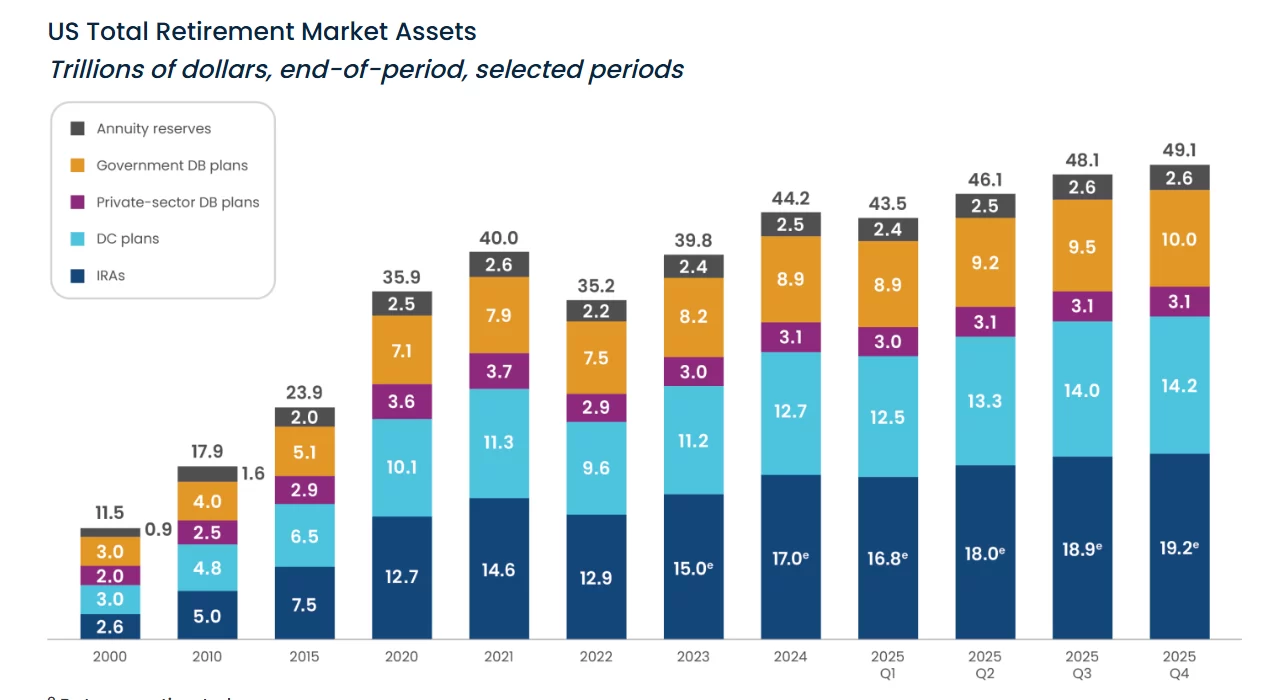

The 401(k) system is vast, with assets counted in the trillions of dollars. According to the latest data published by the Investment Company Institute (ICI) as of April 2026, total retirement assets in the United States surpass $49 trillion. For the first time in history, assets in 401(k) plans alone have exceeded $10 trillion, amounting to $10.1 trillion. These funds serve tens of millions of active participants across the nation.

Within 401(k) plans, asset allocation is dominated by investment funds, accounting for 57 percent ($5.8 trillion) of total assets. Equity funds represent about 33 percent ($3.4 trillion), multi-asset and target-date funds contribute roughly 15 percent ($1.6 trillion), while bonds and cash-like securities make up about 10 percent ($1 trillion). While this allocation is subject to periodic shifts, mutual funds remain the most significant component.

Growth prospects for the 401(k)

With assets reaching $10.1 trillion at the close of 2025, projections from research firms like Cerulli Associates and ICI forecast continued growth for the 401(k) market. Annualized growth rates of seven to nine percent are expected in the coming years, driven by new policy initiatives and favorable economic trends. At this pace, it would not be surprising for total assets in the 401(k) system to reach even higher benchmarks by 2027.

Cryptocurrency’s entry into retirement portfolios

In a move viewed as transformative for both retirement saving and the digital asset industry, the U.S. Department of Labor (DOL) recently issued a rule expanding defined contribution plans’ access to alternative assets, including cryptocurrencies. This regulatory shift follows former President Trump’s executive order in August of last year, which called for expanding retirement participants’ access to alternatives like crypto and real estate.

Lori Chavez-DeRemer, the U.S. Secretary of Labor, explained the motivation behind the policy update in an official statement:

“Our aim is to fulfill President Trump’s commitment to a new golden era by promoting a retirement system that enables more Americans to retire with dignity. This proposed rule will demonstrate how plans can consider products that better reflect today’s investment environment. Greater diversity will foster innovation and represent a major win for American workers, retirees, and families.”

Formally published under the title “Fiduciary Duties in Selecting Designated Investment Alternatives,” the rule grants so-called “Safe Harbor” protections to 401(k) plan managers, enabling them to include assets like cryptocurrencies, private equity, and real estate in their plan offerings. This safe harbor is intended to shield plan administrators from certain legal risks, provided they comply with a set of six guiding criteria. These include requirements for risk-adjusted performance evaluation, reasonable fee assessment, sufficient liquidity, reliable asset valuation, performance benchmarking against relevant indices, and the need for substantive expertise or access to qualified advisors when selecting complex investment products.

- Performance: Expected returns should be evaluated from a long-term, risk-adjusted perspective.

- Fees: Fees must be “reasonable”; there is no longer a requirement to select the lowest-cost option.

- Liquidity: There needs to be adequate cash flow to allow participants to withdraw funds as needed.

- Valuation: Reliable mechanisms are required for fair and timely asset valuation.

- Benchmarking: Asset performance should be compared to appropriate benchmarks with similar risk profiles.

- Competence: Plan managers must understand the complexity of the chosen investment or obtain suitable advice.

These regulatory changes represent a stark shift from the Biden administration’s earlier calls for extreme caution in crypto investments—guidelines that were officially withdrawn in May 2025. The Trump-era regulations seek to expand the menu of asset classes beyond stocks and bonds, providing individual savers with access to alternatives that have long been available to institutional investors.

If even a modest one percent of the $10.1 trillion currently in the 401(k) market were to flow into crypto, this would represent a staggering $101 billion—far surpassing last year’s total inflows into crypto ETFs. Given that not all employers will immediately adopt these investment options, even a more conservative estimate of annual inflows, ranging from $25 to $45 billion over the next 12 to 18 months, would have a significant impact. Much like the rollout of spot ETFs, where early adoption was limited and some major asset managers were initially skeptical, adoption among 401(k) plans is expected to be gradual but could accelerate over time.

A key feature of 401(k) investing is that much of this capital is “sticky” and not subject to frequent selling. This long-term orientation could reduce selling pressure in crypto markets and provide increased support for spot asset prices as new inflows arrive from retirement savers.