Bitcoin kicked off the new week trading at $74,000, with global volatility currently favoring crypto traders. As geopolitical tensions with Iran escalate, diplomatic efforts are underway around the world to halt a broader conflict before it deepens. Even Donald Trump, known for his calls for regime change in Iran, could seek to declare a rapid and limited “victory” should the right circumstances align. Investors and analysts are now left asking: What should we expect in the days ahead?

Central Banks Steal the Spotlight as Iran Crisis Looms

Attention turns to central banks this week, with policymakers set to address the economic fallout stemming from rising Iran-related tensions. In recent days, a detailed calendar of key economic events has shaped market expectations. Now, focus shifts to interpreting these developments, assessing likely outcomes, and preparing portfolios in response to shifting data and projections.

U.S. Industrial Production: A Vital Economic Indicator

The Federal Reserve will publish its monthly Industrial Production report today, measuring real output across U.S. manufacturing, mining, and utilities. As a bellwether of industrial activity and broader economic momentum, the index provides valuable context on demand, resource utilization, and the underlying business cycle.

January’s report showed a modest uptick, reflecting a rebound in manufacturing and steady mining output. Capacity utilization also edged slightly higher, signaling a mild strengthening in the use of available production resources.

Growth is expected to be more subdued this month; however, should output surpass forecasts, industries tied to raw materials and manufacturing could see their stocks receive a much-needed boost. This would, in turn, reduce pressure on the Fed to initiate rate cuts in the immediate term.

By contrast, if today’s figures fall short, the central bank could face rising pressure to cut rates to stimulate economic growth.

U.S. PPI Data Offers Hints on Inflation Outlook

Scheduled for release Wednesday, the Producer Price Index (PPI)—compiled by the U.S. Bureau of Labor Statistics—serves as an advance indicator for consumer price trends, given its focus on underlying cost shifts. Back in January, the PPI reflected only moderate increases in both headline and core measures, with services inflation remaining the primary driver of upward pressure while commodity prices held steady. Despite easing from earlier peaks, inflation in service sectors continued to linger, signaling persistent pricing challenges.

Should the latest figures meet or surpass expectations, the likelihood of the Fed postponing any rate reductions will increase. However, a weaker-than-expected PPI—if reinforced by follow-up PCE and CPI data—could add weight to arguments in favor of cutting rates.

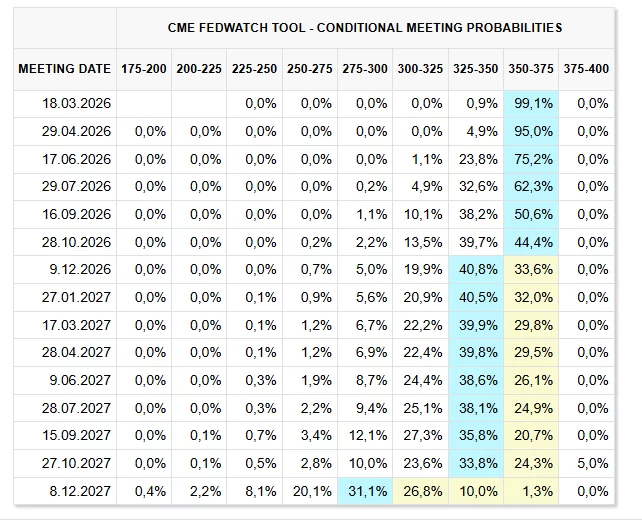

FOMC Decision Poised to Shape Market Sentiment

The Federal Open Market Committee’s (FOMC) upcoming rate decision will be accompanied by its Summary of Economic Projections (SEP), which includes vital growth, inflation, and employment forecasts. In January, the Fed held rates steady, recognizing progress on inflation but highlighting that it still sat above the desired 2% threshold. Policymakers emphasized continued economic resilience and a gradual cooling in the job market, cautioning that further evidence was needed to confirm a sustained downward move in inflation toward target levels.

With the SEP projections, markets will scrutinize any incremental changes in growth and inflation outlooks. The closely watched “dot plot” offers insights on how many rate cuts Fed officials anticipate for 2026. In light of mounting Iran tensions, any hawkish tilt in these forecasts may have outsized influence—especially for crypto markets observing every policy signal for cues.