The US Secretary of State has indicated that Washington will respond to Iran’s proposal either today or tomorrow. But as the conflict drags on, worries of a prolonged war are heightening fears of a looming stagflation—an economic environment marked by stagnant growth and persistent inflation. What does stagflation actually mean? How might it affect stock markets, specific sectors, and especially the world of cryptocurrencies? A report by the UK-based asset management firm Schroders sheds light on these uncertainties, providing context for investors caught between global politics and volatile markets.

What is stagflation?

Rising anxieties over the Iran conflict center on its potential to trigger an energy shock, which in turn could usher in an era of stagflation. Energy prices in Europe have more than doubled, while gasoline costs in the US are nearing their highest levels in recent memory. With Asia struggling to secure energy supplies and a continued closure of the Strait of Hormuz disrupting the flow of products from helium to fertilizer, the consequences ripple across everything from food to semiconductors. This is not just a war with local impacts—it is disrupting supply chains throughout the global economy.

Stagflation typically refers to a situation where real GDP growth falls below its decade-long average, while inflation (as measured by the Consumer Price Index) exceeds its trend. Historically, such conditions have proven especially challenging for equity markets, often regarded as their most unfriendly landscape.

Stocks: navigating sector differences

While stagflation is generally bad news for stocks overall, not all sectors are affected equally. The key consideration is that performance gaps between sectors—and even individual companies—tend to widen under such conditions.

There is an argument that the sector makeup of European exchanges could offer them some relative resilience compared to US markets. Considering the influence of US equities globally, this could pose issues for many investors. Beyond commonly cited valuation arguments, this strengthens the case for a more selective approach, rather than passive global equity strategies, according to Schroders’ analysts.

When economic growth is sluggish, both businesses and consumers tighten their belts, dampening sales and exacerbating unemployment. In such a climate, high inflation only compounds the problem: while companies in a robust economy can typically pass higher input costs on to the consumer, weak demand makes this much harder. As a result, profit margins are squeezed and earnings are pressured downward.

Central banks’ options are also constrained. While interest rate cuts are a typical lever to stimulate demand, high inflation often forces monetary authorities to consider raising rates instead, aiming to rein in price growth. Yet this brings the risk of worsening the downturn. If rates are cut, inflation may flare up further. In effect, policymakers face a difficult balancing act.

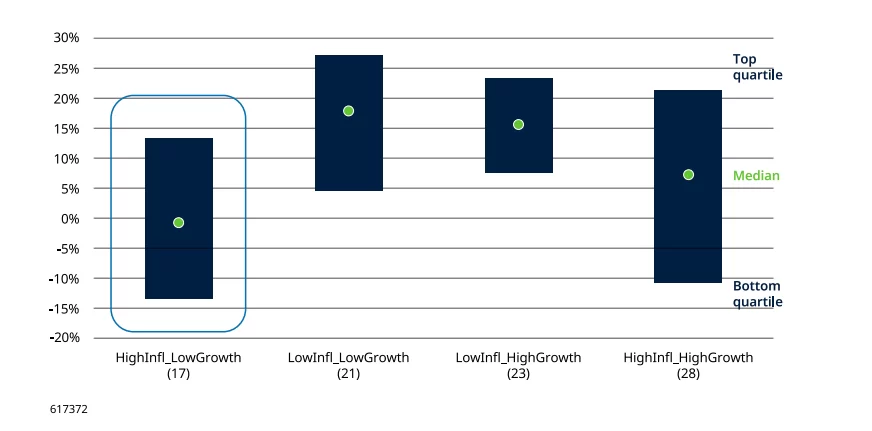

Data dating back to 1926 suggests that median annual real returns for equities during stagflation years have hovered around zero. While this is notably lower than investors’ long-term expectations for stocks, earning a return roughly equal to inflation is not necessarily a catastrophic outcome under adverse circumstances.

Analysts note that in nearly half of stagflation periods, equity returns could be described as the “least bad” scenario. Around half of outcomes fall within a neutral range, with a quarter exceeding it and another quarter performing worse.

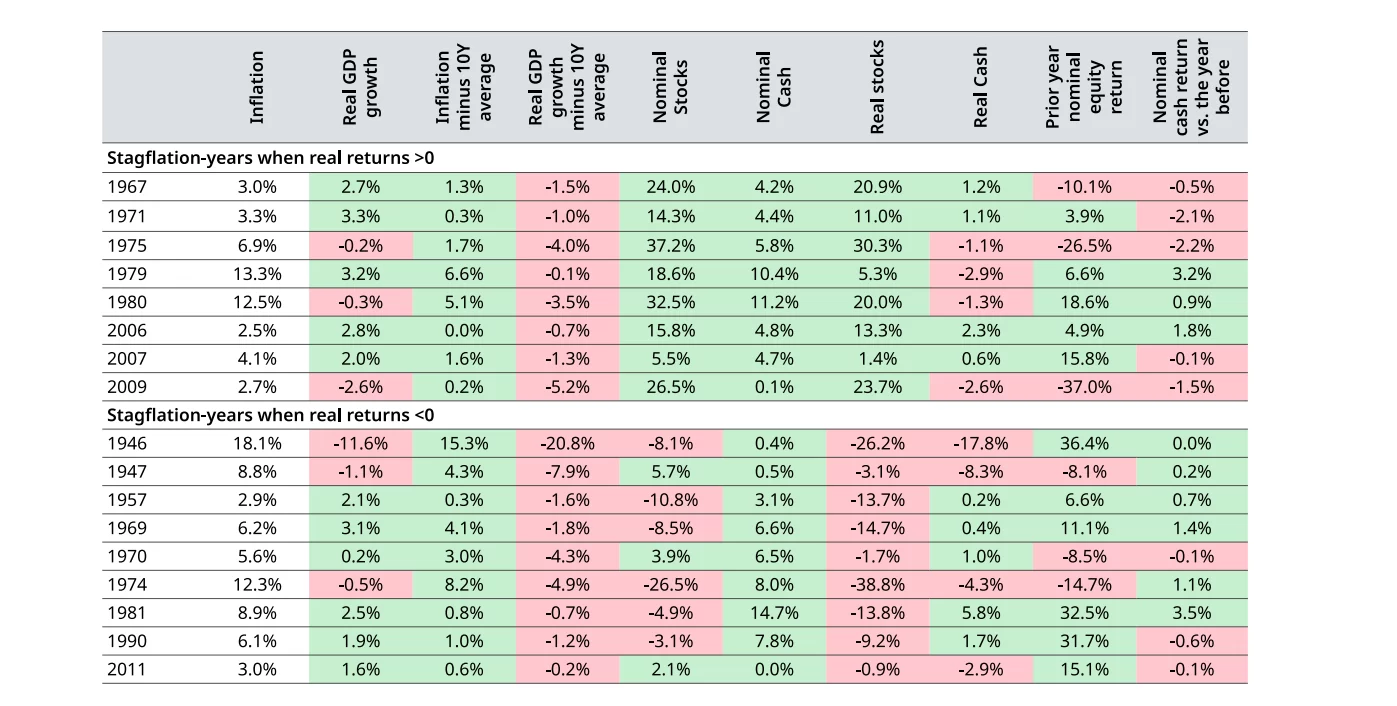

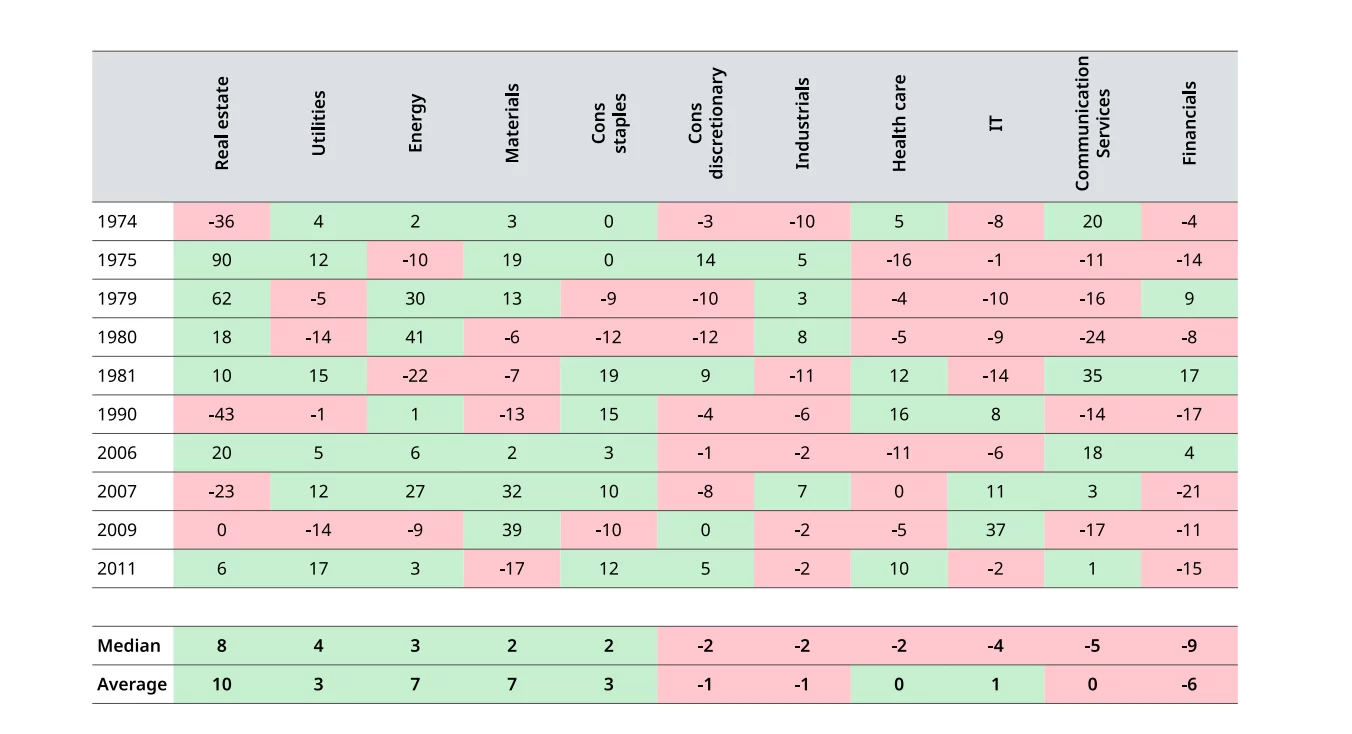

Only in eight separate years since 1926—namely 1967, 1971, 1975, 1979, 1980, 2006, 2007, and 2009—have equities delivered positive real returns during stagflation. As such, bold moves in these periods require careful deliberation by investors.

Analysis shows that positive and negative real returns during stagflation are not closely linked to market performance in the previous year or to shifts in interest rates.

Sector-specific impacts

How do different sectors fare? While sector data has been tracked since 1974, changes in sector composition over time make long-term comparisons challenging. For example, what was once dominated by telecom heavyweights like AT&T now sees tech giants Alphabet (Google) and Meta accounting for nearly three-quarters of the sector’s market capitalization (as of February 28, 2026). These evolving weights mean that historical patterns offer at best limited predictive value.

Recent sector performance reflects this diversity.

Defensive industries such as utilities and consumer staples generally outperform, as their demand is less sensitive to economic cycles. Energy and raw materials companies have also tended to do well during stagflation, since high commodity prices are both a cause and symptom of inflation—something that continues to be relevant in today’s climate.

Interestingly, while healthcare is normally considered a defensive sector—with relatively stable performance—the period from 1974 to 2025 saw healthcare lagging during times of low growth and high inflation.

Real estate, sometimes seen as a “real asset,” can perform relatively well, yet outcomes vary widely depending on factors such as rental agreements, inflation linkage, and debt profiles. Investors in this space must carefully assess tenants’ operational risks—discretionary spending is the first to drop, meaning staples outperform non-essential consumer items.

Both IT and communication services have generally posted weak performance, reflecting a mix of higher input costs and soft demand, but also valuation effects. Since investors expect strong future earnings from IT companies—particularly growth-focused firms—popular names often command high price-to-earnings ratios.

Cryptocurrencies and stagflation

The US stock market is particularly exposed in a stagflation scenario because of its heavy weighting in technology—one of the most vulnerable sectors. Only 15% of US equity benchmark allocations are in sectors that have historically performed well in such environments, raising the likelihood that the index’s fortunes could spill over negatively into the cryptocurrency market.

Japan, too, is at a disadvantage due to its reliance—44% of its listed equities—on globally sensitive industries like manufacturing and luxury goods. If the conflict continues to disrupt energy flows into Asia, renewed debate over “carry trades” could emerge, further putting pressure on the global economy and digital assets like cryptocurrencies.

While Bitcoin briefly stood out amid geopolitical turmoil, reality has set in now that the anticipated disruptions have materialized. The data suggests Bitcoin is neither an inflation hedge nor a safe haven in times of war. Although its performance before and during recent crises has drawn dramatic commentary, as of now Bitcoin has not convincingly demonstrated an ability to hold value under stagflationary conditions.

History shows that stagflation does not automatically spell disaster for financial markets. Yet, if the Fed is slow to cut rates while Europe is forced to tighten policy, this scenario—which is not entirely unlikely—would present real challenges for the US and for risk-sensitive asset classes moving forward.